The growth of private credit to a nearly $2 trillion asset class is a powerful validation of its role in modern finance.1 However, this rapid maturity has fundamentally bifurcated the market: separating the commoditized, large-scale segment that is structurally exposed to risk from the specialized, hands-on segment where true alpha is generated. Recent high-profile losses, often tied to misrepresented collateral or opaque borrower structures in large-scale private credit, are not a failure of the asset class itself, but a predictable consequence of the structural flaws inherent in size.2,3 The core lesson is clear: distance from the borrower ultimately destroys capital.

The Structural Cost of Size

The pressure on mega-funds to deploy vast capital pools has created an operational imperative to chase ever-larger transactions, prioritizing speed and scale over prudence and proximity. This dynamic has produced a systemic drift toward structures that erode lender protections and widen the gap between capital and credit risk.4 The resulting market architecture exhibits three interlocking weaknesses:

- Size and Syndication: The use of large-size club deals or syndicates that increase the number of lender participants, thus diluting the hands-on, bilateral control.

- Covenant Erosion: The acceptance of covenant-lite structures that remove or weaken financial maintenance tests, delaying the lender’s ability to intervene until enterprise value is severely impaired.

- Diligence Compromise: The substitution of comprehensive, continuous asset verification with passive, paper-based review, exponentially increasing exposure to fraud and collateral misrepresentation.

In the vicious cycle of deal size, bigger doesn’t mean better. The velocity required to win large financings has led to process substitution, replacing first-hand collateral verification and continuous monitoring with desktop diligence and reliance on third-party summaries. The result is an environment where representations can outpace reality. The Tricolor alleged fraud case, where collateral was seemingly fabricated, illustrates how procedural shortcuts in high-speed deal environments can transform structural weakness into outright capital impairment.

Yet beyond these individual failures lies a broader paradox: size is self-reinforcing. Large funds must deploy quickly to justify their size, which drives them toward larger loans and broader syndicates, further weakening structure and oversight. As underwriting discipline yields to capital velocity, recovery outcomes tell the story: direct loan recoveries average just 33% upon default, compared to 52% in the syndicated market.5 In theory, size should confer strength; in practice, it often breeds distance, opacity, and fragility.

In many cases, the pursuit of magnitude has come at the expense of mastery. In private credit, control and connectivity, not capital volume, remain the true determinants of resilience. Firms with the ability to maintain bilateral negotiation, rigorous covenant frameworks, and ongoing collateral verification are positioned not only to preserve capital but to exploit the inefficiencies created by scale’s blind spots.

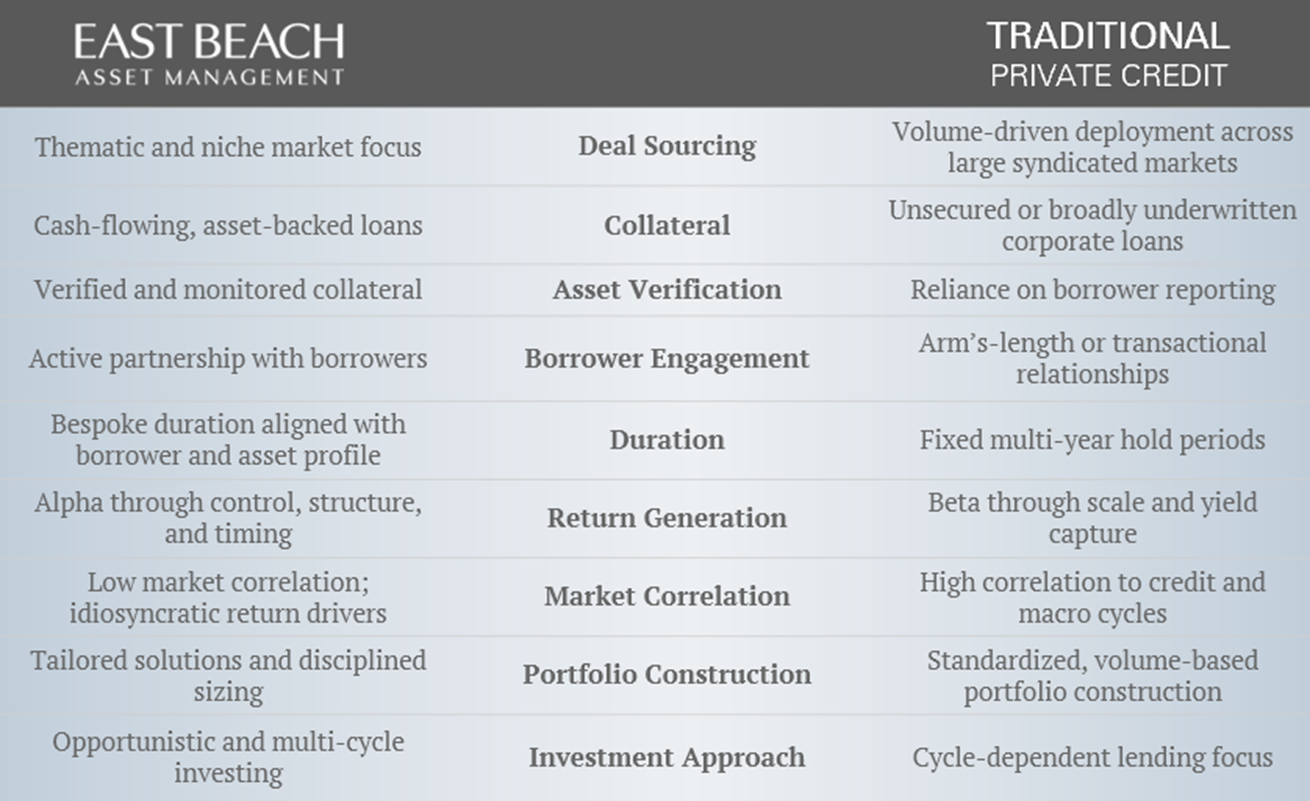

The recent examples of structural failures convey the importance of utilizing creative and sophisticated risk mitigants. Grounded in multi-cycle investment experience, EBAM’s investment strategy incorporates thinking outside of commoditization by prioritizing control, as well as proximity to its borrowers, to support a thoughtful and research-driven investment process. The greatest opportunity in the current cycle lies outside of regular-way, middle-market lending. It exists in underserved and overlooked segments that large, traditional private credit funds cannot efficiently access.

Focusing on capital access challenges and bespoke strategies in opportunistic credit and specialized cash-flowing asset financings allows EBAM to structure highly tailored deals with unique risk profiles. Operating in sectors with fewer comparables and less crowded competition, EBAM can build in favorable terms and greater lender control, positioning the strategy for what we believe are compelling risk-adjusted returns.

EBAM’s advantage stems from a direct relationship model that keeps us close to the assets and borrower. This proximity drives better alignment, faster decision-making, and more bespoke financings tailored to each opportunity.

In a rapidly growing private credit market increasingly defined by size over selectivity, alpha is migrating toward managers who take a hands-on, niche-focused approach, prioritizing alignment, protections, and tailored structuring over speed and scale.

Size can be a double-edged sword: while large funds validate the asset class and provide market liquidity, size often introduces structural separation that increases risk. Strategic differentiation is essential, and firms with multi-cycle experience, operational engagement, and a focus on less crowded segments are often better positioned to identify and structure risk-adjusted opportunities that conventional models may overlook.

Sincerely,

The Team at East Beach Asset Management

Contact

East Beach Asset Management

Rachael Sarabi, Founding Partner

investorrelations@eastbeacham.com

www.eastbeacham.com

Footnotes

- McKinsey, The Next Era of Private Credit.

- Credit Chronometer, Double Trouble in Tricolor: Risks in Collateral Misrepresentation.

- Neuberger Berman, Lessons from First Brands and Tricolor.

- Monetary Fund, Global Financial Stability Report, April 2024: The Rise and Risks of Private Credit.

- Reserve Board, Private Credit: Characteristics and Risks.

- Chronograph, How Direct Lending Competition Is Impacting Private Credit Deal Terms.

- Private Credit Outlook: Keep Calm and Diversify.

- American Investment Council, Private Credit.

Legal Information and Disclosures

This document is being made available for informational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. This memorandum expresses the views of the author(s) as of the date indicated and such views are subject to change without notice. Past performance is not indicative of future results. Investment strategies involve risk, including the loss of principal. Reference applicable disclosures and risk factors before making any investment decision.

Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. East Beach Asset Management, LLC. (“EBAM”) believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

This memorandum, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part, in any form without the prior written consent of EBAM.

© 2025 East Beach Asset Management, LLC.

About East Beach Asset Management

East Beach Asset Management is a privately-owned investment management firm focusing on tactical credit across private and public credit markets. Founded by credit industry veterans Cee Sarabi and Rachael Sarabi, EBAM’s investment platform spans opportunistic credit, structured products and capital solutions. The firm targets outsized returns to investors combined with high margins of safety across all market environments. EBAM’s Partners bring an average of 20+ years of experience across global markets, investing and managing investor capital through various market cycles.

Investor Relations

East Beach Asset Management

investorrelations@eastbeacham.com

Visit us on LinkedIn